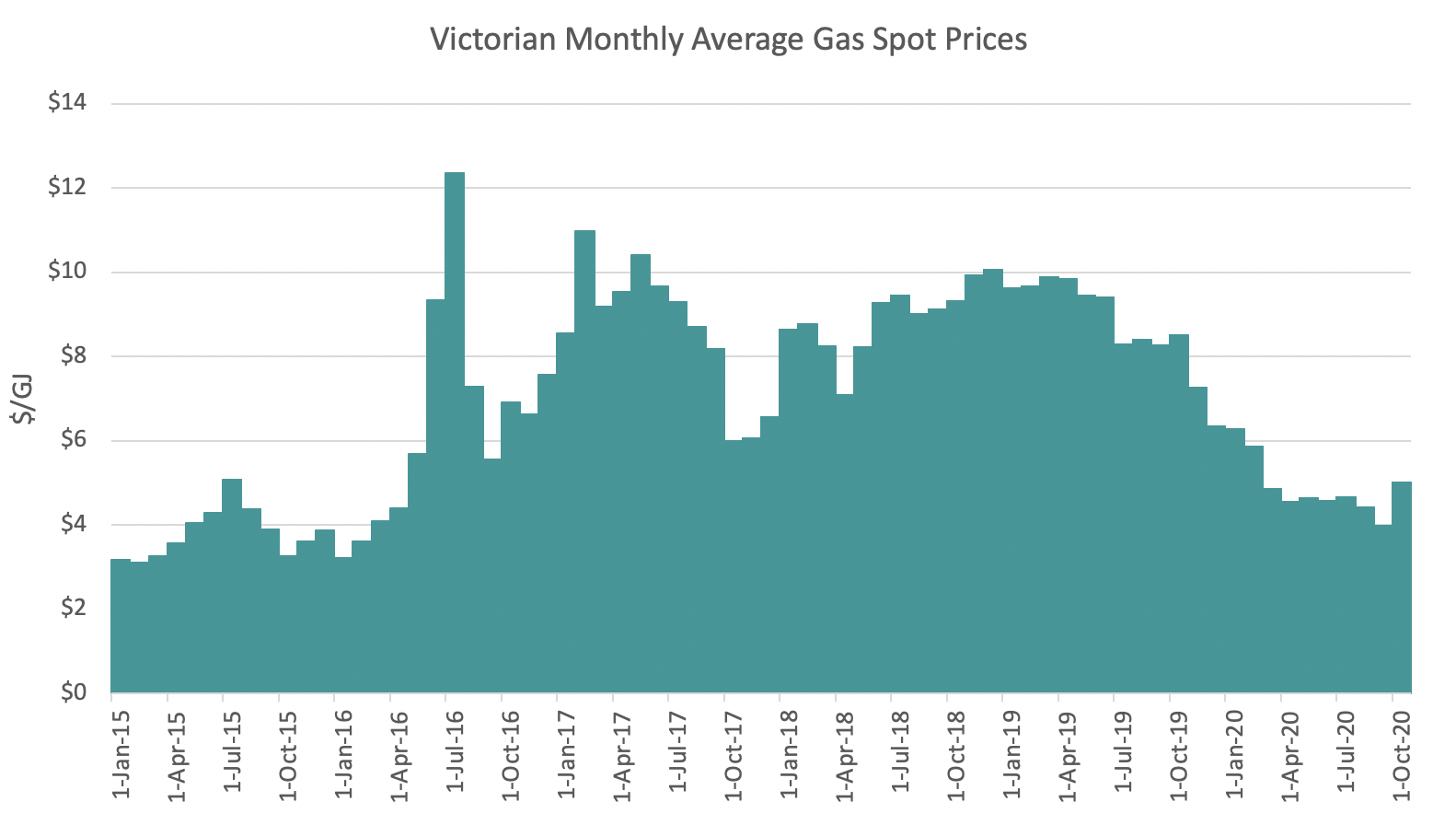

It was not that long ago where conventional wisdom had natural gas prices at least $8/GJ and then tracking above $10/GJ going forward. It is now hard to envisage natural gas prices reaching these now perceived ‘lofty heights’, although it is equally hard to foresee gas prices sitting in the Australian industry desired range of $4 to $6/GJ.

When the Gladstone LNG export terminals became operational, the east coast of Australia natural gas market price reached parity with global LNG prices. Consequently, the traditional circa $4/GJ domestic gas price experienced for many years, became a distant memory as gas prices escalated and ramped-up beginning in winter 2016, and ran through to winter 2019.

Since late 2019, the global LNG marketplace has become more competitive and it was reported that Australia became the largest LNG exporter in 2019 taking over the mantle from Qatar. However, we note that BP reported Qatar slightly ahead of Australian exports.

Nevertheless, global LNG supply increased from Australia, Russia and USA; and demand is now falling evidenced by the International Energy Agency estimation that global gas demand in 2020 will fall by 4% from 2019 levels.

Global natural gas prices have softened due:

- Lower global demand impacted by a historically milder European winter

- Softer oil prices given many LNG contracts are indexed to global oil prices

- Lower demand due to the COVID pandemic as economies have slowed

Looking forward on the global scene, Qatar has plans to increase production by 64% by 2027. It is hard to foresee the global LNG market prices pushing upward soon.

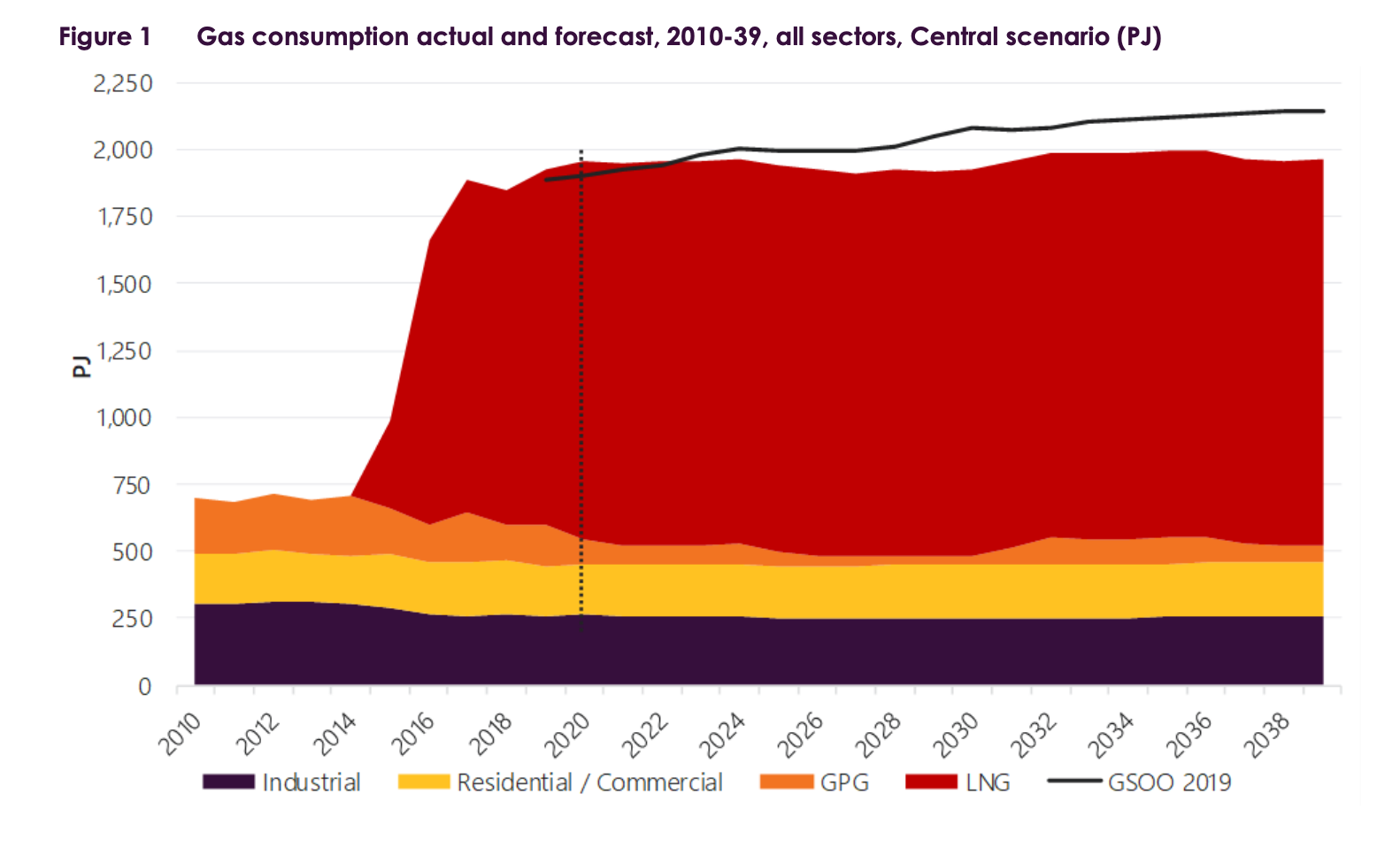

For the east coast Australian domestic gas market, as with any market, there are two sides; namely demand and supply.

Looking at demand-side:

- Gas Powered Generation is expected to decline (see orange band in chart from AEMO’s Gas Statement of Opportunities and confirmed by our own market modelling

- AEMO predicts residential demand to remain constant, but we are not so convinced. With the popularity of roof-top solar and the improvements to heat pump technology, we foresee that gas-heating load is, and will be further challenged, by heat pump technologies. As the export value of Solar PV crashes, and storage becomes cheaper; it is our prediction that heat pumps will impinge upon residential gas heating. The all electric home promoted in the 1970’s, will become fashionable again.

On the domestic supply-side, we have:

- The NSW Narrabri gas field progressing but not yet completed, but assuming it reaches commercial production, Santos estimates the Sydney delivered price to be $6.40/GJ, as compared to the original estimate of $8.70/GJ. Time will tell whether the $6.40/GJ is reality or not.

- The proposed import terminals remain in contention, but it is hard to foresee that the east coast of Australia would have more than one in operation. (i.e This could have been said about Gladstone LNG processing terminals, but there are now 3 in operation today).

The National COVID-19 Coordination Commission (NCCC) was tasked with mobilising the economy to combat the virus and concluded that Australia needs a gas-led recovery and a vision of $4/GJ to $6/GJ gas was conceived. If the life cycle production cost is more than this target, it is hard to foresee gas contract market prices (as distinct from spot prices), being offered to consumers at those levels.

In summary, the Australian east coast gas market prices are unlikely to reach the $10/GJ price level in the next few years, while the expectation of consumers receiving gas offers less than $6/GJ is also considered unlikely. It seems that gas prices over the next few years are likely to hover between these two boundaries.