The last week of November has a history of exhibiting extreme spot prices and this year, was no exception.

There have been about 10 occasions in the market's history when the last week of November has led to extreme prices. However, the one that sticks in my memory is before the NEM started, back in November 1997.

In accordance with our AFSL Authorised Representative obligations we have included a disclaimer and qualified the publisher at the end of this article.

Distant memory ...

For the first time in the market’s short history there was serious price separation between VIC and NSW in November 1997 due to the arrival of hot weather and a VIC to Snowy interconnector outage. During this time, the VIC forward market was at a premium to NSW; but those days are long gone. Consequently, NSW Government owned generators adopted the practice of also selling VIC contracts against the NSW node. The Victorian retailers welcomed their offers as an alternative to the stand-alone poor credit-rated, debt-laden Victorian private generators.

However, when the VIC and NSW prices materially separated for the first time in 1997, the NSW generators were on the wrong side and reportedly lost about $12m across the two days of 25 and 26 November 1997.

And now, November 2024 ...

Back to last week, extreme prices were evident in NSW on Wednesday 27 November and then again in bizarre fashion, on Friday 29 November. Looking at Wednesday you can use the play-back and shows how extreme prices were predicted from about 1:30pm through to 8:00pm, with demand predicted to reach 12,000MW amongst tight reserves. Such an event would have triggered the $600/MWh price administered cap.

A spike occurred at around 3:00pm and a small amount of RERT (i.e. 65MW) was activated and then unregulated demand response caused demand to drop to about 11,000MW. All the remaining extreme prices then faded away.

You can hit the play button and stop at any point, as well as scroll along using the scroll slider.

Taking a look at Friday 29 November, this was a bizarre outlook with demand forecast to only reach less than 9,000MW while extreme prices were predicted to last from 7:00am through to 3:30pm. Another case where the administered price cap would have been triggered.

However, as the day played-out, there was one half-hour spike of about $3,000/MWh at around 7:00am, but then the extreme prices faded away. The team at Watt-Clarity have done some homework on the event and pointed out the AEMO dispatch engine “is forecasting possible outcomes based on one equation in predispatch, but a very different form of equation in dispatch, so the actual outcome in dispatch is that the constraint is not binding anywhere near as much, and so prices are remaining moderate.”

As the playback chart shows below, after the initial spike it all faded away with no doubt many market players hanging onto each 5-minute period as it unfolded.

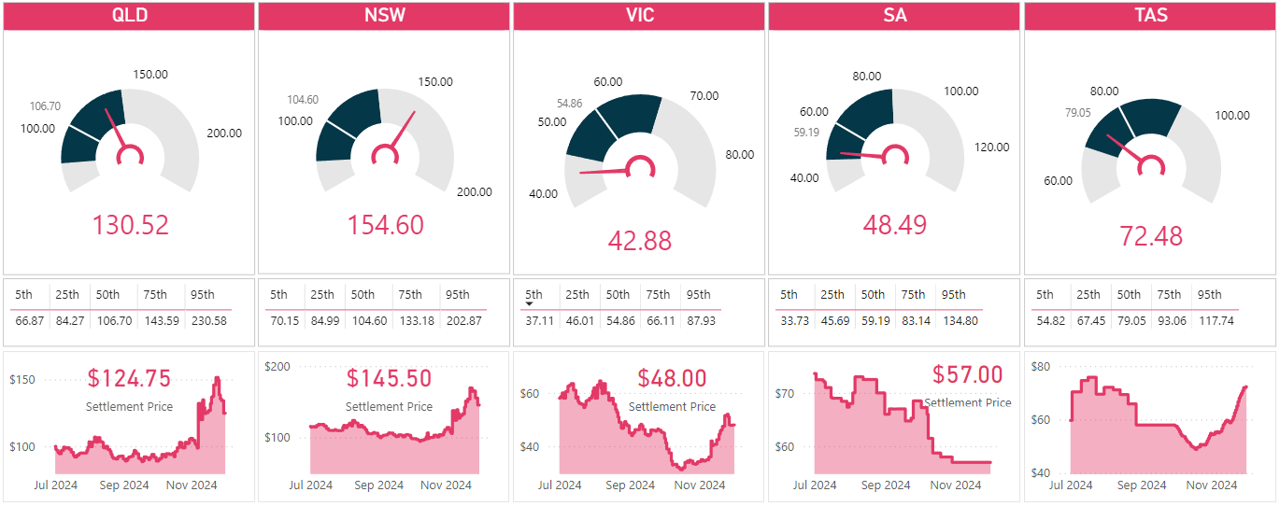

Having a broader look at the quarter, the dials below show our probabilistic spot forecast along with the current quarterly average spot price below each dial.

The observations are:

- QLD actual spot is currently sitting between our 50th and 75th percentile forecast, so nothing too remarkable to report and the higher location has been driven by riding on the back of NSW stronger spot prices. The forward market expects the average to drift down from $130.52/MWh to $124.75/MWh by the end of the quarter. The forward market peaked at $151.50/MWh early last week, but since then has been correcting downward rapidly.

- NSW is tracking in our top quartile of our forecast due to the extreme price days. Last week the forward market peaked at $169.50/MWh and has corrected downward as the threat of sustained high prices faded. The forward market also expects by the end of the quarter to move downward from $154.60/MWh to $145.50/MWh

- VIC has yet to flex it’s muscle this quarter so the average spot price is sitting in our bottom quartile at $42.88/MWh. The forward market has factored in a bit more strength in the spot by trading at $48.00/MWh by the quarter end.

- SA has also been relatively calm so far and is averaging a slight premium to Victoria at $48.49/MWh located just above our 25th percentile forecast. SA has also yet to flex it’s muscle in the spot and the forward market which hasn’t traded for more than a month, is sitting at $57.00/MWh

- TAS is tracking between our 25th and 50th percentile at $72.48/MWh comfortably above the last offered price by HydroTas of just under $58/MWh. By combining the last offer with the actual spot prices during the quarter puts the end of quarter estimate at around $72/MWh which almost matches the current average spot price.

The key percentiles on the dials below are where the dial ranges from the 5th to the 95th percentiles, then the 25th percentile is marked by the start of the dark segment, the 50th is the white line between the dark segments, and finally the 75th percentile is the end of the dark segment.

The area charts below the dial show the journey of the forward price for the quarter since 1 July, and the label shows the current forward price.

Stay tuned to see how the rest of the quarter plays-out and we will make more commentary in our interactive monthly reports available on energybyte.com.au

Disclaimer and Notes

Energybyte is published by Empower Analytics Pty Ltd (ABN 38630239002), Authorised Representative no 1274453 of Capital Treasury Solutions (AFSL 429066). Any questions or feedback must be directed to Empower Analytics Pty Ltd as the sole publisher.

This newsletter contains general information and is not advice to buy or sell any position.

Empower Analytics has exercised professional care in the preparation of this newsletter, the information includes data from third parties which is not independently verified, and it is current at the date of publication. Empower Analytics is under no obligation to update this data.

Before making any trading or investment decision, you should seek professional advice. No liability is accepted for actions or omissions by anyone. Past performance does not predict future outcomes.